Philadelphia

- Published:

- July 3, 2024

Locality: Philadelphia, Pennsylvania (USA)

City Population: 1,584,064 (2019)

Metro Population: 6.1 million (2019)

Plan Title: Housing for Equity: An Action Plan for Philadelphia

Date of Plan: October 2018

Date of Case Study: September 2020

Substantive highlights

Housing for Equity: An Action Plan for Philadelphia was created by the City’s Housing Advisory Board in 2018 as a ten-year plan to increase housing opportunities for residents through the development and rehabilitation of affordable housing.

The plan has five core strategies:

- House the most vulnerable residents

- Preserve and protect long-term affordability

- Provide pathways to sustainable homeownership and wealth creation

- Encourage equitable growth without displacement

- Enable efficient and innovative development and rehabilitation to promote greater housing choice

The quantifiable goals of the plan are to:

- Support new housing for 36,500 households

- Preserve 63,500 households in housing.

The strategies outlined in Housing for Equity will be largely funded by federal programs such as Section 8 Housing Choice Vouchers, CDBG, and the HOME Investment Partnerships program. The City has also proposed local funding for initiatives in the plan, including sales of public land to developers for affordable housing and contributions from private and philanthropic donors. The City also intends to capture a portion of the value generated through allowing increased density of new buildings to source a housing trust fund. Additionally, the City will explore the opportunity to save on healthcare costs by investing in safe, affordable housing, then, in partnership with healthcare providers, redirecting saved healthcare costs to rental assistance programs.

Process

Housing for Equity was developed over the course of several years through a series of housing planning efforts by the City.

In 2015, the City of Philadelphia created the Housing Advisory Board and mandated the development of a multi-year housing plan to maintain and increase the City’s affordable, workforce, and market-rate housing. Developing the plan would include a complete review of the City’s policies and housing studies.

In 2016, the Division of Housing and Community Development and the Philadelphia Housing Authority completed an Assessment of Fair Housing (AFH) with input from almost 5,000 residents. The AFH is a comprehensive assessment of barriers to fair housing in the City and includes a list of recommendations to address those barriers.

Also in 2016, the Mayor convened task forces to address homelessness, evictions, and historic prevention as well as a number of working groups, such as the Access to Homeownership Committee and Construction Cost and New Technology Committee. Each of these groups developed goals and recommended action steps for the City to consider. Combined, the groups developed over 100 recommendations to promote housing affordability and stability. Separately, the Mayor tasked a research and data analysis consultant, PennPraxis, with reviewing housing programs in other cities for lessons that could be applicable in Philadelphia.

In 2018, a consulting team lead by Local Initiatives Support Corporation (LISC) drafted the Housing for Equity plan, which incorporated the recommendations from the AFH, PennPraxis, and the task forces and working groups. LISC shared the draft plan for feedback with the Housing Advisory Board, the Philadelphia City Council, the Philadelphia Association of Community Development Corporations (PACDC), and the AFH stakeholder group in four separate public meetings. The Housing Advisory Board and the Department of Planning and Development edited the plan drafted by LISC, culminating in the publication in the same year of the completed Housing for Equity: An Action Plan for Philadelphia.

Additional detail on the process the City took to develop Housing for Equity, including engaging stakeholders and refining their list of recommendations to the City, is provided in Foundation for the Future: Developing Philadelphia’s Housing Action Plan.

Metrics, targets, and implementation

The Housing for Equity plan has two core quantitative goals for the years 2018-2028:

- Support new housing for 36,500 households. The plan defines a new housing unit as a newly constructed unit or a formerly vacant unit that becomes occupied.

- Preserve 63,500 households in housing. According to the plan, a unit is preserved when occupancy of the unit is maintained through rehabilitation or financial assistance.

The plan refines these two quantitative goals by need and income, specifying that the construction and preservation of a combined 100,000 units shall:

- Newly house 2,500 households experiencing homelessness in rental units.

- Support the creation of new units or preservation of a total of 71,000 existing units for current tenants, including (a) 39,400 units for extremely low-income households (0-30% AMI), (b) 12,200 units for very low-income households (30-50% AMI), and (c) 19,400 units for low-income households (50-80% AMI).

- Support the creation of new units or preservation of existing units for 11,500 current workforce tenants (80-120% AMI).

- Support new housing for 15,000 households in market-rate units (>120% AMI).

Implementation status

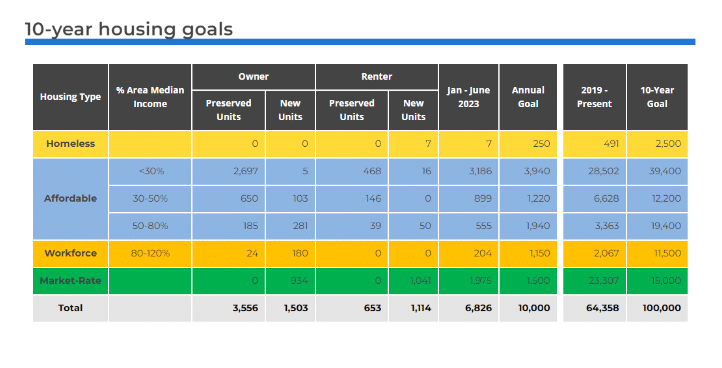

As of June 2023, the most recently available data on Philadelphia’s progress towards its housing goals, the city’s Housing for Equity Housing Action Plan had created or preserved 64,358 homes since 2019, or roughly 64% of its 10-year goal of 100,000 homes.

Philadelphia’s Housing Action Plan Dashboard breaks down the housing the city has built by programs, race and ethnicity, income levels of people served, and by census tract. Between January 2023 and June 2023, Philadelphia’s Housing Action Plan produced or preserved 6,826 units. Of these units, 3,556 were preserved for homeownership, 1,503 were built new for homeownership, 653 were preserved for rentals, and 1,114 were built new for renters.

Of the 1,503 new homeownership units built in Philadelphia between January and July of 2023:

- 5 units were affordable to households making less than 30% AMI.

- 103 units were affordable to households making between 30 and 50% AMI.

- 281 units were affordable to households making between 50 and 80% AMI.

- 180 units were what Philadelphia calls “workforce housing,” meaning they are affordable to households making between 80 and 120% AMI.

- 934 units were market rate.

Of the 1,114 new rental units built in Philadelphia between January and July of 2023:

- 16 units were affordable to households making less than 30% AMI.

- 50 units were affordable to households making between 50 and 80% AMI.

- 1,041 units were market rate.

Coverage of four policy pillars

| Coverage of Four Policy Pillars | Not Covered | Moderate Focus | Substantial Focus |

| Create and preserve dedicated affordable housing units | – | – | ✓ |

| Promote affordability by reducing barriers to new supply | – | ✓ | – |

| Help households access private-market homes | – | ✓ | – |

| Protect against displacement and poor housing conditions | – | ✓ | – |

Participating agencies

| Participating Agencies | No Role | Supporting Role | Leading Role |

| Office of the Mayor | – | – | ✓ |

| Office of the City/County Manager | ✓ | – | – |

| Housing Department | ✓ | – | – |

| Planning Department | – | ✓ | – |

| Development Agency | – | ✓ | – |

| Permitting/Inspections Department | – | ✓ | – |

| Finance/Tax Department | ✓ | – | – |

| City/County Council | – | ✓ | – |

Policy tools

Housing our most vulnerable residents

- Develop an Emergency Homelessness Prevention Program with Flexible Rental Assistance modeled on the New York City HomeBase initiative. This program uses a data-informed assessment tool to provide flexible financial assistance and wraparound services to prevent shelter entry.

- Expand Adaptive Modifications Program (AMP) to make more homes accessible. AMP provides City-funded adaptations to a house or apartment that allow easier access and indoor mobility.

- Initiate an Eviction Prevention Program to resolve landlord-tenant disputes without displacement. If the landlord files suit, the program will provide legal support to eligible low-income tenants in housing court. Further legislation should require the landlord to disclose the reason for lease termination.

- Explore the Nexus between Health and Housing to identify cost saving interventions. Data will be used to have discussions with healthcare providers to support investment in housing.

- Seed a Flexible Housing Subsidy Pool to finance supportive programs. Utilize a portion of healthcare cost savings to seed a funding pool to augment funding of new and existing rental assistance programs.

- Advocate for Sufficient Housing Choice Vouchers to increase housing opportunities for very low-income households. This Program will be used to target housing for households at or below 30% AMI.

Preserving and protecting long-term affordability

- Establish a Housing Accelerator Fund to preserve affordable housing. Local housing dollars will provide a one-time capital infusion, leveraging it to attract social impact capital.

- Expand Credit Enhancement Product to increase workforce housing. The Philadelphia Redevelopment Authority (PRA) is piloting a $1 million credit enhancement that covers the first 25% of defaulted construction loans for developers who build workforce housing affordable to households earning up to 120% AMI.

- Expand Small Landlord Repair Program Pilot. The PRA will provide a loan-loss reserve fund to private lenders who make loans of up to $25,000 for repairs to rental properties (four or fewer units) for households at or below 100% of AMI. One third of loans must serve households at or below 50% AMI.

- Expand and Modify the Shallow Rent Subsidy. Use the Flexible Housing Subsidy Pool to fund a shallow rent subsidy ($300 per month for a period of up to one year) to households undergoing a housing crisis.

- Strengthen Expiring Use Regulations. Require owners of subsidized rental housing to notify the City, housing advocates, and tenants before the property’s affordability period expires. Establish a Right of First Refusal.

- Utilize the Value of Publicly Held Land as collateral for financing to develop and preserve affordable housing.

- Preserve Existing PHA Units. PHA and the City will continue to partner to preserve units through recapitalization and conversion to project-based assistance under Rental Assistance Demonstration (RAD).

Providing pathways to sustainable homeownership and wealth creation

- Continue Home Repair Grant and Loan Programs such as the Basic Systems Repair Program (BSRP), the Weatherization Assistance Program (WAP), and the Home Preservation Loan Program (HPLP). The City will consider recoverability mechanisms, like attaching a lien to homes repaired via BSRP, to ensure long-term affordability.

- Expand Tangled Title Program to ensure access to housing resources by allowing legal services agencies to provide free representation to homeowners seeking clear title to their homes.

- Consider Waiving Realty Transfer Tax to eliminate a key barrier for first-time homebuyers meeting defined income requirements.

- Continue Mortgage Foreclosure Prevention Program to keep households in their homes by pausing the foreclosure process.

- Expand Closing Cost and Down payment Assistance for first-time, and low- and moderate-income homebuyers. Increase funding to the Settlement Assistance Grant Program and create a new loan fund to cover up to $10,000 of closing and down payment costs.

- Expand Access to Mortgage Financing. The City will work with lending institutions to develop innovative financial products for households with low credit scores or a lack of credit history and encourage lenders to explore alternative credit histories.

- Expand Housing Counseling and Education to ensure successful homeownership through pre- and post-purchase counseling.

Encouraging equitablegrowth without displacement

- Create a Stable Funding Stream for Housing Strategies. Pursue a per-night surcharge on short- and medium-term rentals such as those leased through Airbnb and Flip Key. Research the impact of increasing eviction filing fees.

- Plan for Growth. Zone for greater density in neighborhoods with strong markets and for transit-oriented development (TOD) near transit access points.

- Capture the Value Created by Up-Zoning or Increases in Allowable Density to fund the Housing Trust Fund (HTF). Explore the use of a “special assessment” on the increased value due to up zoning or density increase.

- Continue Homeowner Tax Relief Programs to protect against growth-driven displacement.

- Explore Tax Rebate for Landlords with Permanent Affordable Units with the Department of Revenue, Office of Property Assessment, and State agencies the potential to create a tax rebate like the Homestead Exemption for landlords with nonsubsidized affordable units.

- Allow for Accessory Dwelling Units (ADUs) to generate passive income.

- Leverage Publicly Held Land by selling to developers at a nominal or below-market price in exchange for commitment to produce affordable housing. Prioritize the acquisition of tax-delinquent parcels in high-value neighborhoods.

- Continue to Preserve Long-Term Affordability in Strengthening Markets by continuing large-scale community revitalization efforts such as the Choice Neighborhood Initiative in North Central, the Blumberg Sharswood project, and the revitalization of Bartam Village with the goal of preserving/redeveloping units on a one-for-one basis.

Enabling efficient and innovative development/rehabilitation to promote greater housing choice

- Fully Fund and Implement eCLIPSE (an electronic development permit management system) for the Department of Licenses and Inspections (L&I) within 12 months and ensure that all relevant agencies use the platform for permit reviews shortly thereafter.

- Establish an Affordable Housing Labor Rate by adopting a Project Labor Agreement that would allow a lower union wage rate for affordable housing projects in line with the federal wage rate.

- Promote Modular Construction Technology. Collaborate with L&I staff to accommodate modular permitting and work with investors to develop mechanisms that incentivize financing modular construction

- Seek Flexibility in Energy and Size Requirements. In partnership with HUD and the PA Housing Finance Agency (PHFA), commission a cost-benefit analysis to compare upfront capital costs with long-term operating costs of complying with mandated unit sizes and Passive House specifications.

- Pool LIHTC Preservation Project. Workshops and trainings will be offered to owners and asset managers of low-income housing tax credit projects to build their shared capacity and increase the viability of using 4% tax credits.

- Promote Greater Housing Choice. Explore potential changes to zoning and building codes to facilitate a broad variety of housing types.

Income groups targeted

| Income Groups Targeted | Little/No Focus | Moderate Focus | Substantial Focus |

| 0-30% AMI | – | – | ✓ |

| 30-60% AMI | – | – | ✓ |

| 60-80% AMI | – | – | ✓ |

| 80-120% AMI | – | – | ✓ |

| Market Rate | – | – | ✓ |

Key policy objectives or issues addressed

Which linkages are addressed

- ✓ Healthcare

- ✓ Transportation

Which local funding sources are proposed?

- ✓ In-kind provision of land

- ✓ Private and philanthropic sector contributions, including contributions from healthcare providers

- ✓ Accelerator Fund to attract private investment

- ✓ Housing Trust Fund